Posted on

July 14, 2026

by

Hafez Panju

1 Bedroom/1 Bath 633 sqft Offered at $378 800 Click for more info Enjoy the peace & tranquility this area has to offer. UniverCity at SFU is Vancouver’s premier lifestyle neighborhood. Welcome to this 1bed/1bath/633sqft home, located in Origin, one of SFU’s greenest buildings. You won’t be disappointed. Perfect for investors, first time buyers, students & everyone else in between. Features: freshly painted, open layout, spacious kitchen w/breakfast bar, SS appls, & quartz counters, hydronic heated floors, covered balcony & office nook. The bedroom has...

Posted on

July 13, 2026

by

Hafez Panju

Vancouver, BC – July 13, 2026. The British Columbia Real Estate Association (BCREA) reports that 7,225 residential unit sales were recorded in Multiple Listing Service® (MLS®) Systems in June 2026, up 0.9 per cent from June 2025. The average MLS® residential price in BC in June 2026 was down 0.8 per cent at $946,878 compared to $954,712 in June 2025. Total MLS® residential sales dollar volume was $6.84 billion, up 0.1 per cent from the same time the previous year. BC MLS® unit sales were 18.4 per cent lower than the ten-year average for the month of June. “Sales rose year-over-year in June for the...

Posted on

July 7, 2026

by

Hafez Panju

Welcome to Novo 2 at SFU by renowned builder Intergulf. This bright and well-designed 1 bedroom + den, 1 bathroom home offers 660 sq ft of comfortable living space in the heart of the vibrant UniverCity community. Featuring an open-concept layout with modern finishes, spacious kitchen, and versatile den perfect for a home office or guest space. Enjoy fantastic building amenities including a fully equipped gym and a meeting/party room available to reserve for family gatherings and events. Just steps to SFU, University Highlands Elementary, Nesters Market, restaurants, cafes, scenic walking and biking...

Posted on

July 3, 2026

by

Hafez Panju

VANCOUVER, BC – July 3, 2026 – Demand for all home types in Metro Vancouver* increased to start the summer, with home sales up nearly ten per cent year-over-year in June. The Greater Vancouver REALTORS® (GVR) reports that residential sales in the region totalled 2,390 in June 2026, a 9.6 per cent increase from the 2,181 sales recorded in June 2025. This was 12.4 per cent below the 10-year seasonal average (2,728). “June saw a pattern of broad gains in home sales across all home types relative to the same time last year, which has been a rare occurrence in recent years,” said Andrew Lis, GVR chief...

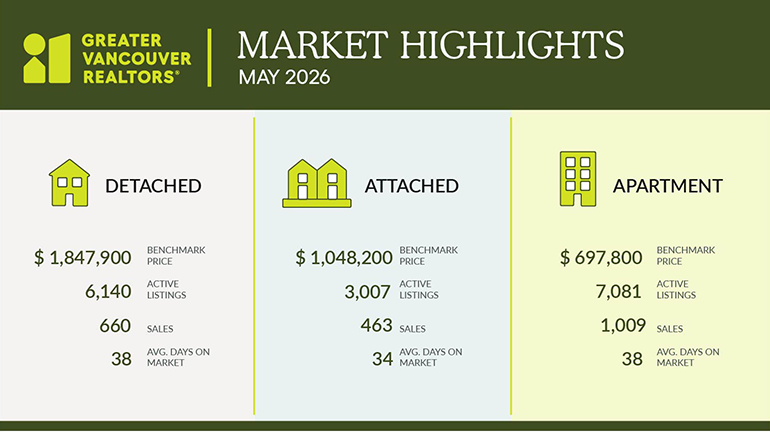

Posted on

June 12, 2026

by

Hafez Panju

Vancouver, BC – June 11, 2026. The British Columbia Real Estate Association (BCREA) reports that 6,790 residential unit sales were recorded in Multiple Listing Service® (MLS®) Systems in May 2026, down 2 per cent from May 2025. The average MLS® residential price in BC in May 2026 was down 1.4 per cent at $945,878 compared to $959,216 in May 2025. Total MLS® residential sales dollar volume was $6.42 billion, down 3.4 per cent from the same time the previous year. BC MLS® unit sales were 26.39 per cent lower than the ten-year average for the month of May. “Rising mortgage rates and a weak labour market...

Posted on

June 2, 2026

by

Hafez Panju

1 Bedroom/1 Bath 633 sqft Offered at $398 800 Click for more info Enjoy the peace & tranquility this area has to offer. UniverCity at SFU is Vancouver’s premier lifestyle neighborhood. Welcome to this 1bed/1bath/633sqft home, located in Origin, one of SFU’s greenest buildings. You won’t be disappointed. Perfect for investors, first time buyers, students & everyone else in between. Features: freshly painted, open layout, spacious kitchen w/breakfast bar, SS appls, & quartz counters, hydronic heated floors, covered balcony & office nook. The bedroom has...

Posted on

June 2, 2026

by

Hafez Panju

VANCOUVER, BC – June 2, 2026 – Led by slow sales in the apartment segment, home sales registered on the MLS® in Metro Vancouver* were down nearly four per cent in May compared to last year. The Greater Vancouver REALTORS® (GVR) reports that residential sales in the region totalled 2,150 in May 2026, a 3.5 per cent decrease from the 2,228 sales recorded in May 2025. This was 26.6 per cent below the 10-year seasonal average (2,930). “While attached sales held relatively steady and detached sales edged up roughly one per cent in May, apartment sales were down about seven per cent year-over-year, which...

Posted on

May 14, 2026

by

Hafez Panju

Top Floor, Corner Home 3 bedroom/2bath/1218 sqft Bright, spacious & open layout are just a few ways to describe this home. This 1218sqft/3bed/2bath, top-floor, corner unit offers southern views & over-height ceilings. Your wait is over. Features: open living & dining rooms, excellent room separation, spacious kitchen with eating area, SS apps, covered balcony & cozy gas F/P. The large primary bedroom has ensuite w/soaker tub & walk-in closet. The well-sized 2nd & 3rd rooms complete this home. Bonus: 2 parking & 1storage locker. Located in Harmony at the Highland;...

Posted on

May 14, 2026

by

Hafez Panju

Vancouver, BC – May 11, 2026. The British Columbia Real Estate Association (BCREA) reports that 6,311 residential unit sales were recorded in Multiple Listing Service® (MLS®) Systems in April 2026, down 1.9 per cent from April 2025. The average MLS® residential price in BC in April 2026 was up 0.8 per cent at $952,768 compared to $944,796 in April 2025. Total MLS® residential sales dollar volume was $6.01 billion, down 1.1 per cent from the same time the previous year. BC MLS® unit sales were 25.38 per cent lower than the ten-year average for the month of April. “Challenges in the local economy and...

Posted on

May 11, 2026

by

Hafez Panju

Loft Style Home at Veritas Excellent Condition 1 Bed 757sqft Priced at $488,000 Click here for more… Stunning! Just one way to describe this south facing loft style home with amazing natural light. Welcome to UniverCity at SFU, Vancouver's premier lifestyle neighborhood. Enjoy the peace & tranquility this area offers. This 1bed/1bath/757sqft home will not disappoint. Features: 17'+ ceilings, freshly painted, new light fixtures, an abundance of light, quality flooring, open layout, SS appls, plenty of cupboard & counter space, spacious living & dining areas. The primary bedroom offers plenty...

Posted on

May 8, 2026

by

Hafez Panju

Thank you to my clients for your continued trust and support—it’s a privilege to help you achieve your real estate goals. I’m truly grateful for the opportunity to work with each of you!

Posted on

May 5, 2026

by

Hafez Panju

1 Bed, 1 Bath, 633sqft Priced at $418,800 Click for more … Enjoy the peace & tranquility this area has to offer. UniverCity at SFU is Vancouver’s premier lifestyle neighborhood. Welcome to this 1bed/1bath/633sqft home, located in Origin, one of SFU’s greenest buildings. You won’t be disappointed. Perfect for investors, first time buyers, students & everyone else in between. Features: freshly painted, open layout, spacious kitchen w/breakfast bar, SS appls, & quartz counters, hydronic heated floors, covered balcony & office nook. The bedroom has pass...

Posted on

May 5, 2026

by

Hafez Panju

Home sales registered on the MLS® in Metro Vancouver remain relatively flat compared to April last year, but a divergence is emerging between market segments. The Greater Vancouver REALTORS® (GVR) reports that residential sales in the region totalled 2,110 in April 2026, a 2.5 per cent decrease from the 2,163 sales recorded in April 2025. This was 22.9 per cent below the 10-year seasonal average (2,735). “Last month we noted that a divergence was emerging between sales trends in the detached and multi-family segments, which continued in April,” said Andrew Lis, GVR chief economist and vice-president...

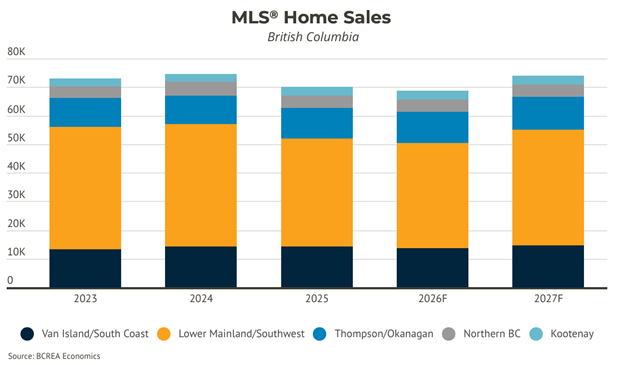

Posted on

April 27, 2026

by

Hafez Panju

BCREA 2026 Second Quarter Housing Forecast Vancouver, BC – April 27, 2026. The British Columbia Real Estate Association (BCREA) released its 2026 Second Quarter Housing Forecast today.

Multiple Listing Service® (MLS®) residential sales in BC are forecast to fall 2.1 per cent to 68,700 units this year. In 2027, MLS® residential sales are forecast to move higher, rising 7.7 per cent to 74,000 units. “The housing market continues to be challenged by persistent global headwinds and a struggling economy,” said BCREA Chief Economist Brendon Ogmundson. “However, improved affordability in many markets combined...

Posted on

April 20, 2026

by

Hafez Panju

Loft Style Home at Veritas Excellent Condition 1 Bed 757sqft Priced at $488,000 Click here for more… Stunning! Just one way to describe this south facing loft style home with amazing natural light. Welcome to UniverCity at SFU, Vancouver's premier lifestyle neighborhood. Enjoy the peace & tranquility this area offers. This 1bed/1bath/757sqft home will not disappoint. Features: 17'+ ceilings, freshly painted, new light fixtures, an abundance of light, quality flooring, open layout, SS appls, plenty of cupboard & counter space, spacious living & dining areas. The primary bedroom offers plenty...

Posted on

April 17, 2026

by

Hafez Panju

Vancouver, BC – April 15, 2026. The British Columbia Real Estate Association (BCREA) reports that 5,766 residential unit sales were recorded in Multiple Listing Service® (MLS®) Systems in March 2026, down 3.6 per cent from March 2025. The average MLS® residential price in BC in March 2026 was down 2 per cent at $939,846 compared to $959,236 in March 2025. Total MLS® residential sales dollar volume was $4.21 billion, down 5.6 per cent from the same time the previous year. BC MLS® unit sales were 34.53 per cent lower than the ten-year average for the month of March. “Global conflict leading to rising...

Posted on

April 7, 2026

by

Hafez Panju

Top Floor, Corner Home 3 bedroom/2bath/1218 sqft $669,800 Open House - Sunday, April 12th 2pm - 4pm Click here for more …. Bright, spacious & open layout are just a few ways to describe this home. This 1218sqft/3bed/2bath, top-floor, corner unit offers southern views & over-height ceilings. Your wait is over. Features: open living & dining rooms, excellent room separation, spacious kitchen with eating area, SS apps, covered balcony & cozy gas F/P. The large primary bedroom has ensuite w/soaker tub & walk-in closet. The well-sized 2nd & 3rd rooms complete this home. Bonus:...

Posted on

April 7, 2026

by

Hafez Panju

1 Bed, 1 Bath, 633sqft Priced at $434,000 Click for more … Enjoy the peace & tranquility this area has to offer. UniverCity at SFU is Vancouver’s premier lifestyle neighborhood. Welcome to this 1bed/1bath/633sqft home, located in Origin, one of SFU’s greenest buildings. You won’t be disappointed. Perfect for investors, first time buyers, students & everyone else in between. Features: freshly painted, open layout, spacious kitchen w/breakfast bar, SS appls, & quartz counters, hydronic heated floors, covered balcony & office nook. The bedroom has pass...

Posted on

April 3, 2026

by

Hafez Panju

VANCOUVER, BC – April 2, 2026 – Home sales registered on the MLS® in Metro Vancouver* continue evolving at a pace similar to last year, with the sales down roughly three per cent from last March. The Greater Vancouver REALTORS® (GVR) reports that residential sales in the region totalled 2,032 in March 2026, a 2.8 per cent decrease from the 2,091 sales recorded in March 2025. This was 31.8 per cent below the 10-year seasonal average (2,981). “Year-to-date, sales are tracking our forecast for the year closely, and the weakness in demand we continue to observe at the aggregate level is unsurprising,”...

Posted on

March 24, 2026

by

Hafez Panju

Top Floor, Corner Home 3 bedroom/2bath/1218 sqft $689,800 Open House - Saturday, April 4th 2pm - 4pm Click here for more …. Bright, spacious & open layout are just a few ways to describe this home. This 1218sqft/3bed/2bath, top-floor, corner unit offers southern views & over-height ceilings. Your wait is over. Features: open living & dining rooms, excellent room separation, spacious kitchen with eating area, SS apps, covered balcony & cozy gas F/P. The large primary bedroom has ensuite w/soaker tub & walk-in closet. The well-sized 2nd & 3rd rooms complete this home. Bonus:...

|