Highlights:

- National home sales rose 2.3% month-over-month in February.

- Actual (not seasonally adjusted) monthly activity came in 40% below February 2022.

- The number of newly listed properties dropped 7.9% month-over-month.

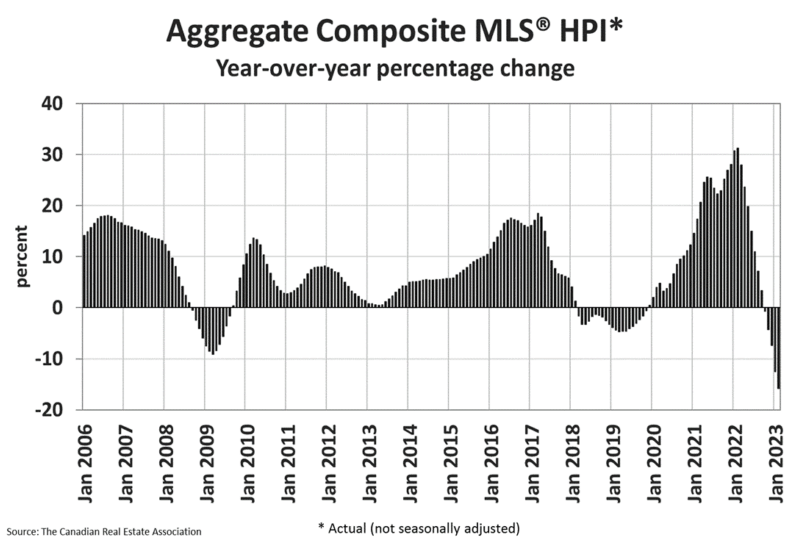

- The MLS® Home Price Index (HPI) edged down 1.1% month-over-month and was down 15.8% year-over-year.

- The actual (not seasonally adjusted) national average sale price posted an 18.9% year-over-year decline in February.

Home sales recorded over Canadian MLS® Systems posted a 2.3% increase from January to February 2023. Gains were led by the Greater Toronto Area (GTA) and Greater Vancouver.

The actual (not seasonally adjusted) number of transactions in February 2023 came in 40% below an incredibly strong month of February in 2022. The February 2023 sales figure was comparable to what was seen for that month in 2018 and 2019.

“February’s data contained the potential of a more robust market to come, but to repeat the bottom line from last month, we won’t know what the 2023 market has in store until the spring,” said Jill Oudil, Chair of CREA. “While we’re not seeing it in the sales or listings data just yet, I would expect homeowners are getting properties ready for the market and prospective buyers are getting mortgage pre-approvals. Make sure to contact your local REALTOR® for information and guidance about buying or selling a property,” continued Oudil.

“The similarities between 2023 and the recovery year of 2019 continued to emerge in February, with sales up, the market tightening, and month-over-month price declines getting smaller,” said Shaun Cathcart, CREA’s Senior Economist. “But the biggest similarity was a sharp drop in seasonally adjusted new listings. Future sellers, many of whom will also be buyers, are likely biding their time until the optimum time to list and buy something else. For most, that’s in the spring. Will buyers jump off the fence to snap homes up in 2023 once they finally start to hit the market? They did in 2019.”

The number of newly listed homes dropped 7.9% on a month-over-month basis in February, led by double-digit declines in several large markets, particularly in Ontario.

With new listings falling considerably and sales moving higher in February, the sales-to-new listings ratio jumped to 58.4%, the tightest since last April. The long-term average for this measure is 55.1%.

There were 4.1 months of inventory on a national basis at the end of February 2023, down from 4.2 months at the end of January. It was the first time the measure has shown any sign of tightening since the fall of 2021. It’s also a full month below its long-term average.

The Aggregate Composite MLS® Home Price Index (HPI) was down 1.1% on a month-over-month basis in February 2023, only about half the decline recorded the month before and the smallest month-over-month drop since last March.

The Aggregate Composite MLS® HPI now sits 15.8% below its peak level, reached in February 2022.

Looking across the country, prices are down from peak levels by more than they are nationally in most parts of Ontario and a few parts of British Columbia, and down by less elsewhere. While prices have softened to some degree almost everywhere, Calgary, Regina, Saskatoon, and St. John’s stand out as

markets where home prices are barely off their peaks. Prices began to stabilize last fall in the Maritimes. Some markets in Ontario seem to be doing the same now.

The actual (not seasonally adjusted) national average home price was $662,437 in February 2023, down 18.9% from the all-time record in February 2022 but up more than $50,000 from its January level resulting from outsized sales increases in the GTA and Greater Vancouver, two of Canada’s most active and expensive housing markets. Excluding these two markets from the calculation cut almost $135,000 from the national average price in February 2023.

Provide by: CREA